The Government Just Made Buying Your First Home More Affordable (And A Few Tips To Make It Even More So)

Buyer Sonja Bush May 23, 2024

Buyer Sonja Bush May 23, 2024

No matter how much buying a house makes sense for your long-term financial well-being, buying your first house can often just seem expensive and totally out of reach. That leads to many younger people putting off buying a home until later in life than they might have, if the costs were lower.

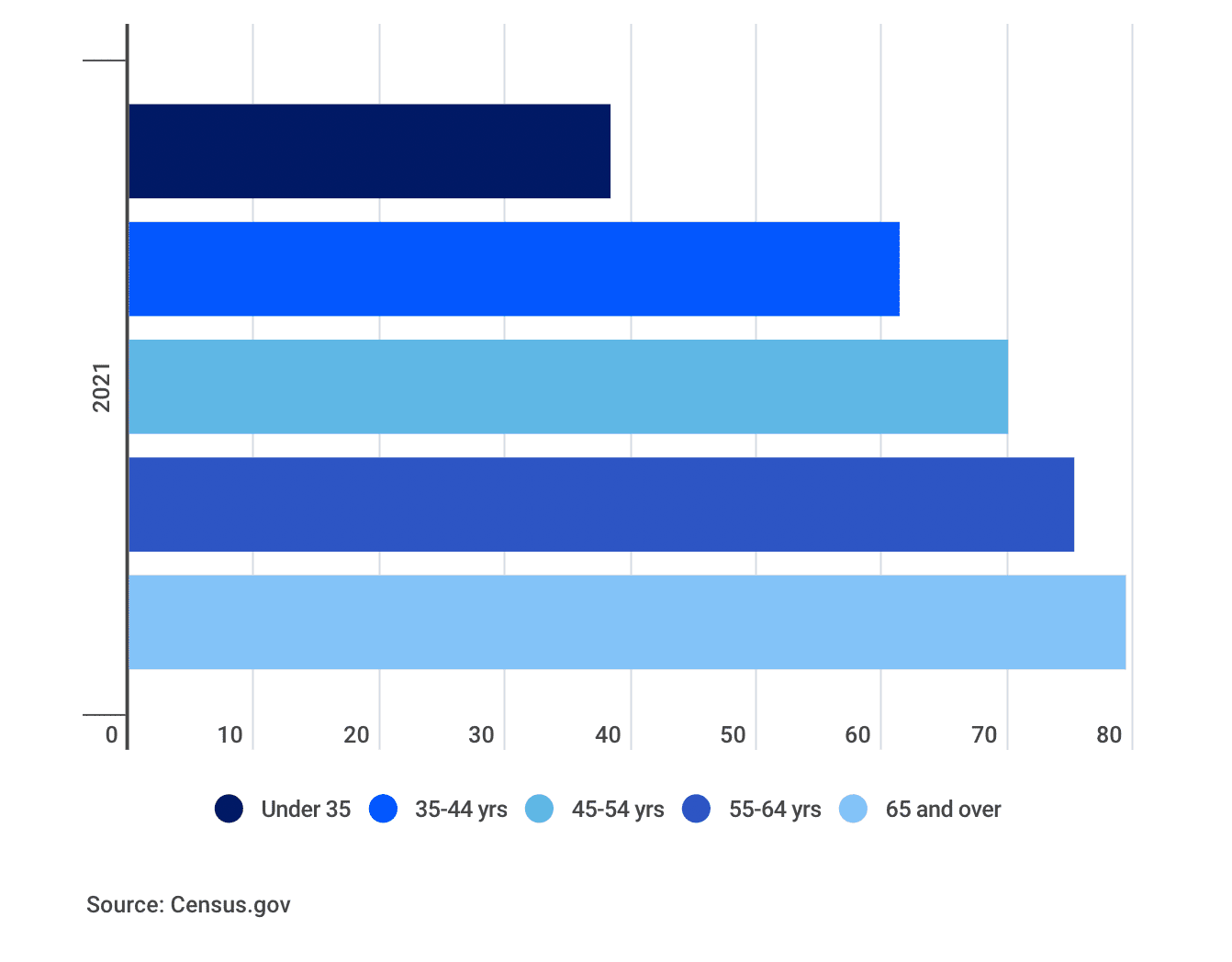

But there are plenty of younger people buying homes. Nearly 40% of people under 35 own a home, so it’s by no means impossible or entirely unaffordable.

As you can see in the graph above, the homeownership rate goes up to just over 60% for those between the ages of 35-44, which is about where the homeownership rate is for the entire US, regardless of age.

Interestingly, if you look at the chart below, the homeownership rate has actually hovered between 62 and 68 percent since 1965. So, basically, the wheelhouse for homeownership begins around 35 years old.

This means that buying a home when you’re under 35 gives you some precious years of building equity, wealth, and long-term financial well-being, while your peers are still renting, or living at home.

Buying your first home is about to become a little more affordable due to a recent move by the Department of Housing and Urban Development (HUD), through the Federal Housing Administration (FHA), to reduce how much mortgage insurance premiums are for FHA borrowers.

FHA loans are a common type of mortgage for many first-time buyers. They are insured by the federal government, and have less strict guidelines, which are helpful for a buyer with lower credit score, or a lower down payment to buy a home. However, when you put a lower down payment on a home, you have to pay mortgage insurance. The premiums for that mortgage insurance is what the FHA is lowering, and they will now be $800 less per year on average.

Not a bad chunk of change to save on a yearly basis. That said, it might seem like a drop in the bucket of what you’d need in order to make buying a home affordable.

If you want to join the ranks of the approximately 40% of younger homeowners, here are a few other ways to shave down the cost of buying your first home and making it even more affordable:

Combining a few of those tips—along with the lower mortgage insurance premiums—will go a long way in making it more affordable to buy your first home now, rather than years from now.

The Takeaway:

Buying your first home is about to become a little more affordable due to a recent move by the Department of Housing and Urban Development (HUD), through the Federal Housing Administration (FHA), to reduce how much mortgage insurance premiums are for FHA borrowers by $800 per year on average.

While that may not seem like enough money to make buying your first home more affordable, you can shave down and control the cost on your own by:

- Not buying too big of a house

- Being flexible on where you buy

- Staying within a budget when furnishing it

- Learning how to do some repairs to it on your own.

Buyer

Buyer

Real Estate

Buyer

Condo

Real Estate

Mammoth Lakes Community

Buyer

Real Estate Education

You’ve got questions and we can’t wait to answer them.